Option Repricing

Originally a thread on X/Twitter:

At a startup, stock options can be lucrative depending on the success of the company.

With valuations down, Founders are asking to reprice historical options.

Here’s what it means, why it’s important and when it’s appropriate.

Cash governs almost everything that a startup does. It impacts the pace of investment in product improvements. It impacts the amount a company can invest in growth. And it impacts how much runway a company has before it needs to raise more capital.

As a result, most startups preserve cash by paying employees lower than market salaries and then add equity-based incentive compensation to pay packages. The value of the equity is usually worthless if a startup fails but it can be extremely valuable if a startup succeeds.

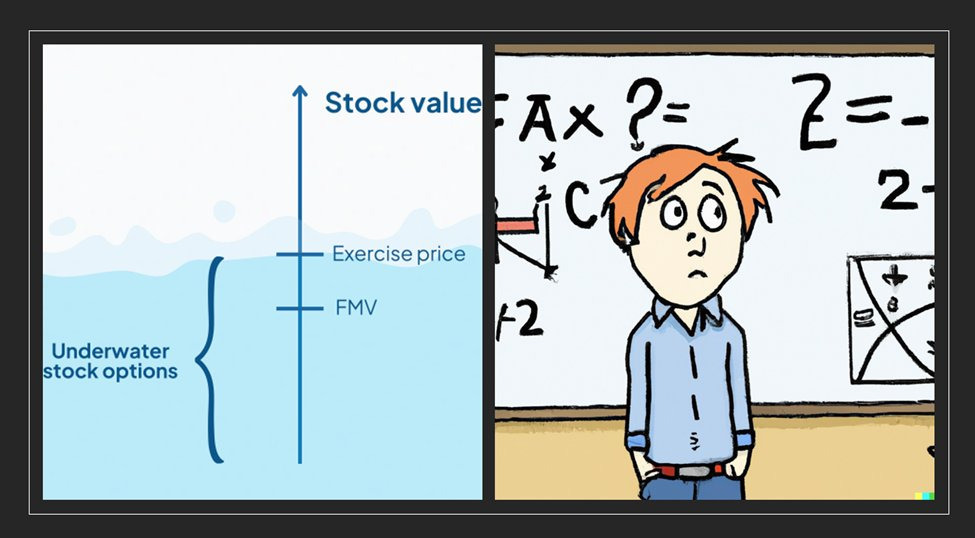

Equity is typically granted in the form of a 7-10 year option to buy common stock at a strike price that’s usually pegged to the fair market value (FMV) of a share of common stock.

The most common determinant of FMV is a company’s “409A Valuation”.

A 409A valuation is done by a 3rd party by analyzing the company’s financial statements, projections, market conditions, and other relevant factors and is primarily used for tax purposes.

But it’s been adopted as “standard practice” for setting the strike price of options.

The why is simple: Setting the strike price at or above the 409A value means that from an accounting perspective nothing of immediate value has been given to an employee and therefore there are no taxes due upon issuance.

If a startup goes public or sells to a strategic, employees can exercise their options and benefit from the difference between the price of the liquidity event and the strike price of their options.

The math is simple: Employees want a low strike price and a high sales price.

Example: If an employee received 1,000 options with a strike price of $5 a share and their startup sold for $15 a share then the employee would cash out $10,000 at time of sale. If the strike price had been granted at $1 a share then the employee would cash out $14,000.

This works well when the value of a startup keeps going up over time because early employees are rewarded with options that have lower strike prices than later employees.

But tangible problems can emerge if a company’s 409A valuation goes down over time.

Problem #1

Employees could view their historical options grants as “worthless” if the new 409A valuation has fallen significantly. This can drive attrition if employees don’t see a short-term path to the value of the company exceeding the exercise price of their options.

Problem #2

If the new 409A valuation is less than the previous 409A valuation it can create feelings of unfairness among employees because new employees will be granted options with greater upside potential than employees that have been around a while.

While repricing historical options can be used to solve these problems, it does come with a cost because repricing is a direct transference of value from investors to employees.

Every dollar that an employee benefits is a dollar that comes out of investor returns.

The conceptual disconnect is that repricing employee options decreases potential investor returns at a time when everyone agrees that the company has lost value!

This disconnect leads to some heated discussions in Board rooms about when repricings are and aren’t appropriate!

Consideration #1

If options are granted with long vesting schedules (i.e. – 4 years) and refreshes are only granted occasionally (i.e. – refreshes at full vesting), there’s a strong case to be made to reprice recent grants of underwater options down.

Consideration #2

A repricing event can be justified on the basis of a Board’s fiduciary responsibility to maximize shareholder value. There are times when a repricing can significantly reduce the risk of employees looking for better opportunities or morale impacting results.

Consideration #3

If the likely exit scenario is a sale to “recoup investor capital”, repricing options incents employees to maximize value to an acquirer. Options will have no value until investors get their money back but employees will benefit from additional value created.

TL;DR: Options have become an important part of compensation in the startup world. Options repricing is a tool that can be used by a company’s Board to correct for obvious inequities as well as to incent and retain employees. But repricings should be the exception, not the rule.

And if you enjoyed reading this, it would be helpful to like, comment and/or share the first post. The X/Twitter algorithm has been unpredictable recently but engagement seems to help!